ECommerce is increasingly international and offers retailers great opportunities – but also uncertainties. Brexit in particular is causing uncertainty for online retailers, as new tax regulations for marketplaces and their own online stores make financial accounting more difficult. JTL-Wawi and the FIBU interface JTL 2 DATEV help online retailers to book their sales quickly, easily and correctly.

Online business recently reached a peak in 2020 – additionally driven by the coronavirus pandemic. According to a Eurostat survey, one in seven internet users in the EU-27 countries made online purchases from companies in 2020. But it is not just the EU member states that are an important sales market for online retailers. The UK is one of the leaders in online business: 90% of consumers there bought from online marketplaces and online stores in 2020. However, Brexit, which was completed on January 31, 2020, has massively changed the sales conditions for retailers.

Great Britain is a third country - customs formalities are necessary

Following a transition phase, the UK has been a third country for tax and customs purposes since January 1, 2021. This affects all trade between Germany and the UK, i.e. the export of goods to the UK, imports to Germany and trade in goods from Germany via the UK to other countries. For the movement of goods, this change primarily means customs controls. The only exception is Northern Ireland. Although Northern Ireland forms the United Kingdom with Great Britain, a special regulation applies: the country will continue to be treated as if it were part of the European customs territory.

If you are an online retailer trading with the UK in the future, you must register your company with the customs authorities and apply for a new EORI number for the UK. The EORI number is the successor to the customs number and is valid at EU level. It is intended to facilitate automatic customs clearance and serves to identify companies. However, existing registrations and VAT IDs will remain valid. As with other third countries, customs declarations with the necessary import declarations are required. Traders have a grace period until January 1, 2022 to set up these new processes: only then will the complete import declaration for standard goods be due. The original deadline of July 2021 has thus been postponed by six months. However, controlled goods such as alcoholic beverages subject to excise duty or certain chemicals have been subject to the direct full customs declaration since the beginning of this year. Simplifications for these goods are only possible with customs authorizations. However, basic simplifications for import clearance ultimately only apply to companies based in the UK.

Taxes are paid differently

There are also further changes to tax. If you sell products to the UK, they are now taxable there from the first penny. The more favorable treatment of minor goods under GBP 15 has been history since the beginning of the year. The value of the goods in pounds sterling is decisive for the tax payable in the UK. Up to GBP 135, UK VAT is payable at the point of sale. If the value exceeds GBP 135, you must pay UK import VAT and customs duties directly to customs. The sales channel determines how VAT is reported and paid at the point of sale: If you sell goods via an online marketplace, the marketplace will collect and pay the VAT directly. However, if you sell via your own store, you must report and pay the VAT yourself.

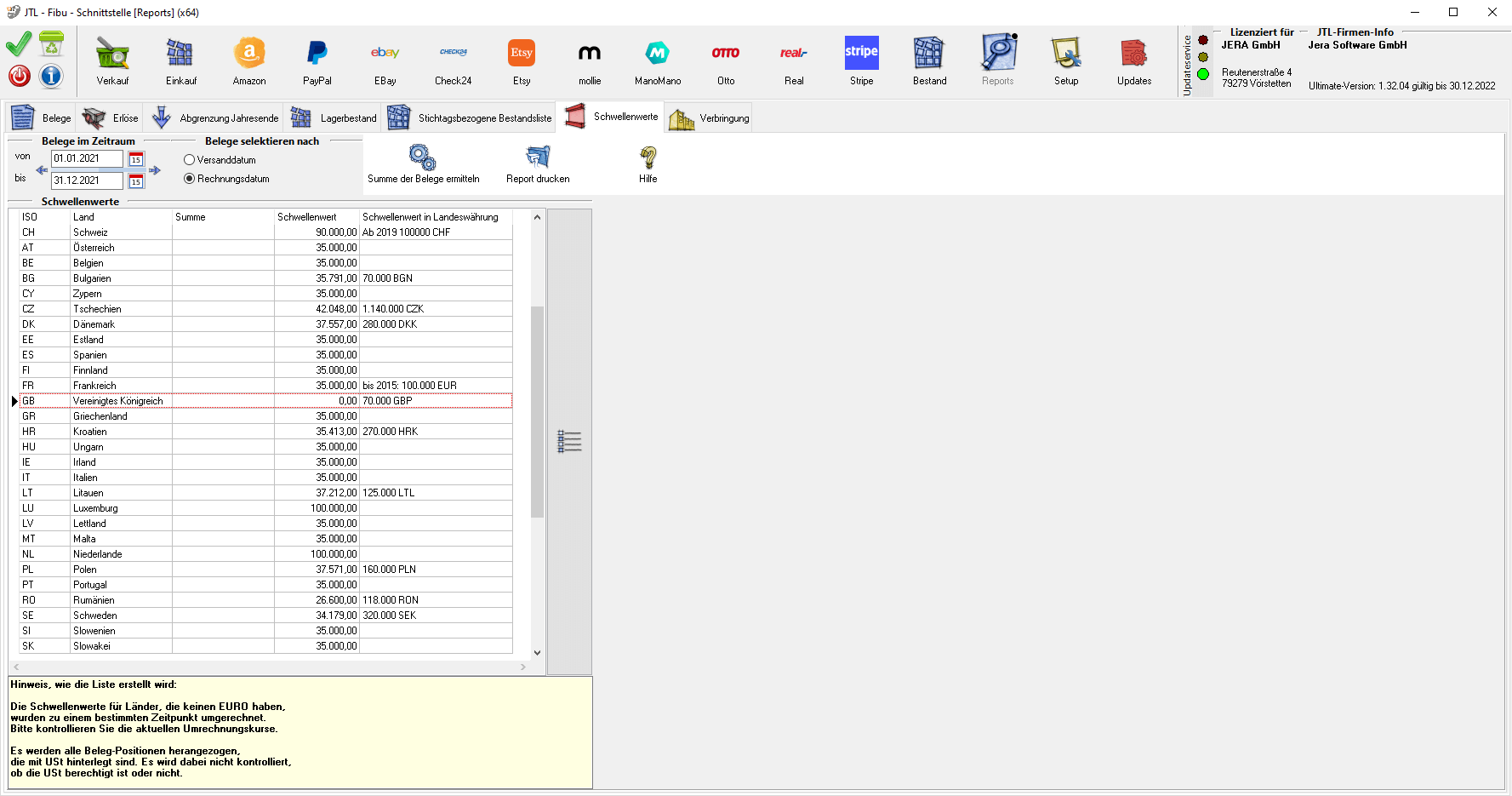

Financial accounting: Post revenues with zero percent sales tax

The new regulations naturally have an impact on financial accounting in eCommerce. But what exactly should you be aware of now as a result of Brexit? As the UK will be treated as a third country, this means for your accounting that revenues from British trade must be posted without VAT and invoices must be shown with zero percent VAT. You will also need to set up a separate revenue account. JTL-Wawi and the FIBU interface JTL 2 DATEV will help you with the changeover. In JTL-Wawi, you adjust the country data and tax administration so that Great Britain is treated as a third country in JTL 2 DATEV. This means that documents are automatically created with zero percent VAT. You use the separate revenue account to report all your revenues to your tax advisor for the payment of VAT in the UK.

JTL 2 DATEV helps with correct financial accounting

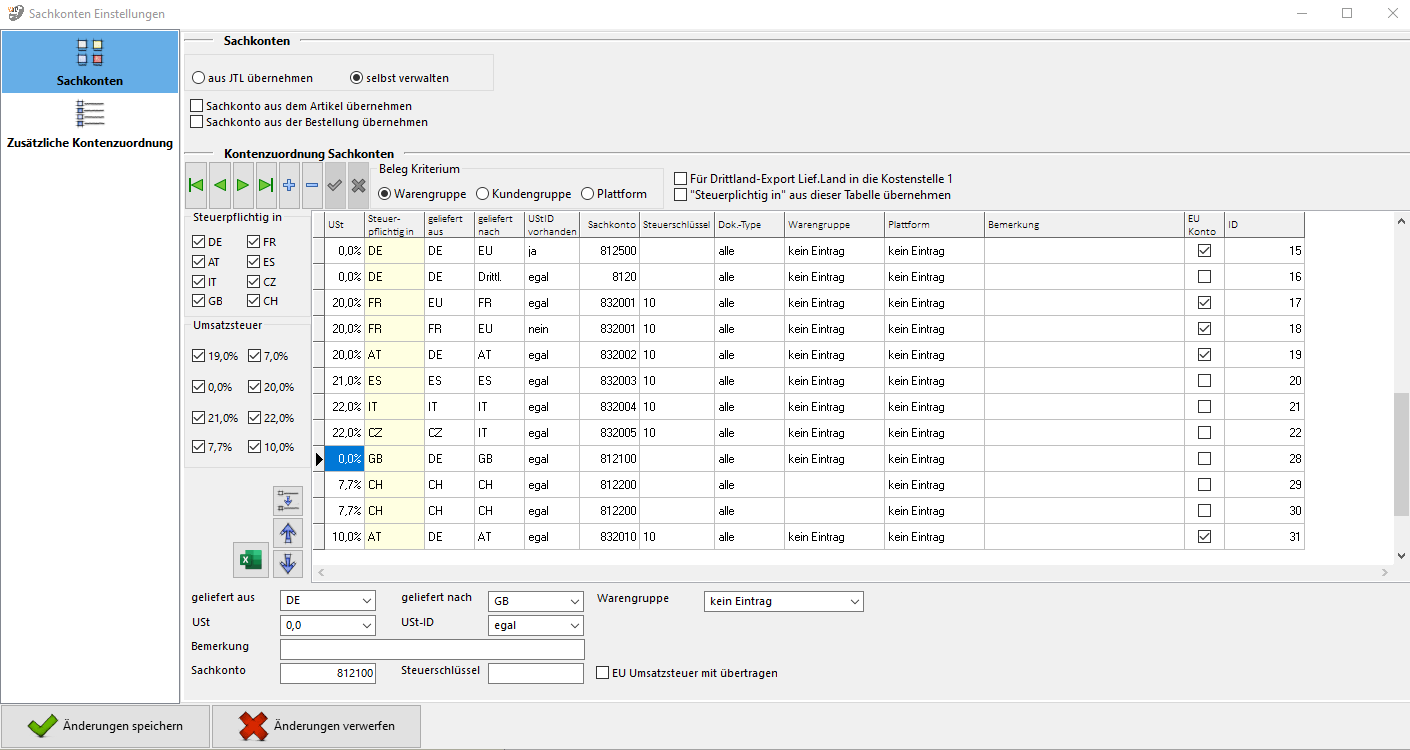

However, due to the different treatment of online stores and online marketplaces, there is a risk of double taxation. The reason: online marketplaces, such as Amazon and eBay, already pay VAT. However, you as a retailer log in all sales, including those of the online marketplaces. To avoid double payments, the VAT already paid by online marketplaces must therefore be offset. In JTL 2 DATEV, you use a separate account for UK marketplace revenues, in which the VAT paid is stored. If you use a tax service such as DutyPay or amavat, additional columns are available to report the taxes already paid. JTL 2 DATEV can automatically fill in these new columns.

As usual, the FIBU interface ensures that the payment data for Great Britain is reconciled with JTL-Wawi and the customer and invoice numbers are assigned to the transaction. At the same time, JTL 2 DATEV automatically generates documents with zero percent VAT using the new country settings from JTL-Wawi and ensures that revenue is reported cleanly to your tax advisor in the form of booking batches in DATEV format. With a separate revenue account for online marketplaces, you can offset taxes that have already been paid and thus avoid double payments.

ConclusionBrexit makes things more complicated. But with the right tools and a little know-how, it’s all doable. The opportunities of the UK market and the customers there generally outweigh the disadvantages. However, you should review your tax situation with your tax advisor in advance and also consider whether the costs and benefits are in proportion. It is also important: Stay up to date. Many commercial cases have not yet been conclusively clarified. However, the topic of accounting can be easily mastered with JTL-Wawi and the FIBU interface JTL 2 DATEV.