Accounting in Germany is facing a significant change: from January 1, 2025, all companies subject to VAT will be required to be able to receive and process e-invoices. This change marks an important milestone in the digitalization of accounting and will permanently change the way invoices are handled. It particularly affects companies in the B2B sector and requires them to deal with the new requirements at an early stage. But what exactly is behind e-invoicing, why is it being introduced and how can companies prepare for the upcoming changes?

In this first article from our three-part blog series on the topic of e-invoicing, you will receive a comprehensive introduction and assistance. We explain what an e-invoice is, which legal principles apply, which goals and advantages the digitization of accounting brings with it and how you can optimally adapt your company to the new regulations. You can also find further assistance and tools from the JTL Group for implementing the new regulation on our information page on the e-invoicing obligation from 2025.

Blog post in short & crisp:

From January 1, 2025, all B2B companies subject to VAT must be able to receive and process e-invoices. This change will bring greater efficiency, transparency and sustainability, but requires timely preparation. Traditional PDFs or paper invoices do not meet the requirements – only machine-readable formats such as XRechnung or ZUGFeRD are considered e-invoices.

We at the JTL Group support you with the JERA E-Invoice 2 FIBU solution, which makes receiving, validating and archiving e-invoices simple and legally compliant. Start now to be optimally prepared!

What is an e-bill? Definition and legal basis

The e-invoice is much more than a PDF document that is sent by email. The term refers to a structured, electronic data format that has been specially developed for the automated processing of invoices.

From XML to ZUGFeRD - when to use what?

The main difference lies in the data structure. An e-invoice is created in XML format, which corresponds to the EU DIN 16931 specifications. This structure allows invoice data to be imported directly into accounting systems without having to be entered manually. This makes the entire process, from checking and account assignment to archiving, more efficient and error-free. In addition to the XRechnung, a purely machine-readable format, the hybrid ZUGFeRD format is also permitted, which, like a PDF, is also clearly visible to human readers.

The legal basis for e-invoicing is set out in EU Directive 2014/55/EU and the Growth Opportunities Act. These regulations oblige companies to be able to receive e-invoices from 2025. For companies in the public sector, e-invoicing has already been in force since 2020, and this obligation is now being extended to all B2B companies in Germany.

Why is e-billing becoming mandatory? Goals and advantages of digitization

Reducing bureaucracy: The first priority is to increase efficiency. Manual handling of invoices is time-consuming, error-prone and cost-intensive. E-invoices eliminate these problems by automating the entire invoice processing procedure. Data is taken directly from the invoice, checked and processed without any manual input.

Sustainability: Switching to paperless invoices saves millions of sheets of paper. Companies that digitize their processes contribute to reducing their ecological footprint. This meets the growing expectations of customers and partners to operate more sustainably.

Tax transparency: The automated processing and validation of invoice data makes it easier for the tax authorities to combat tax fraud. At the same time, companies benefit from an improved overview and traceability of their business transactions.

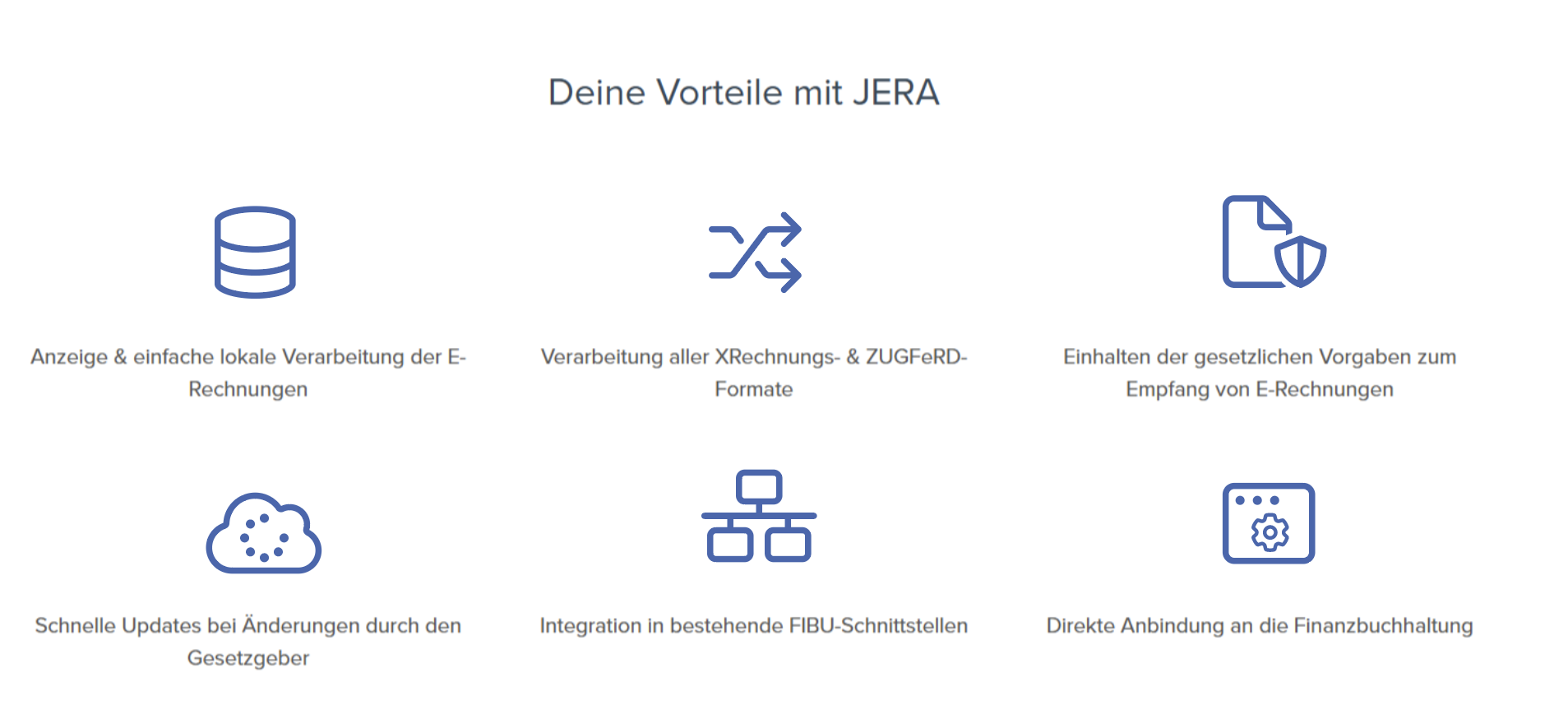

Smooth management of e-invoices with JERA

Switching to e-invoicing may seem complex at first glance, but with the right tool, the transition will be smooth. At JTL Group, we offer comprehensive solutions to support you in implementing and optimizing your e-invoicing processes. With the e-invoice 2 FIBU solution from JTL subsidiary JERA, you can receive, validate and archive e-invoices and integrate them directly into your accounting systems. The software fulfills all legal requirements and facilitates compliance with the new regulations.

You can use the JERA tool both as an add-on to existing accounting systems and as a standalone solution, depending on your requirements.

Who is affected? Overview of the new obligations for companies

The e-invoicing obligation affects:

- All companies in Germany that are active in the B2B sector.

- Large corporations as well as small and medium-sized enterprises.

- Small businesses that are exempt from VAT under Section 19 UStG, as they must receive e-invoices from suppliers and service providers.

Reasons for the obligation for small businesses:

- Suppliers and service providers could issue e-invoices from 2025. It must be possible to process these technically.

- For the B2C sector: No obligation to use e-invoices. Nevertheless, it makes sense to standardize processes and also issue e-invoices to end customers. Advantage: Reduced internal effort and consistent processing.

Exceptions relieve small businesses

- Small-value invoices up to 250 euros and tickets

- Tax-free sales in accordance with Section 4 UStG – These exemptions are intended to relieve the burden on smaller companies in particular and facilitate the introduction of e-invoicing.

Webinar: E-invoicing obligation 2025: basics & best practices for online retailers

08.01.2025, 11:00 a.m.

E-invoicing will be mandatory from 2025 – are you ready? In our webinar, you will learn everything you need to know about the legal basis for mandatory e-invoicing for online retailers. We will also show you how to send e-invoices directly from JTL-Wawi and how to receive, check and process them in a legally compliant manner with the new JERA solution “E-Invoice 2 FIBU”. Take the opportunity now to prepare yourself optimally and digitize your accounting processes!

Speaker: Johannes Seidel, Managing Director JERA GmbH

Transition periods and exceptions: What applies when?

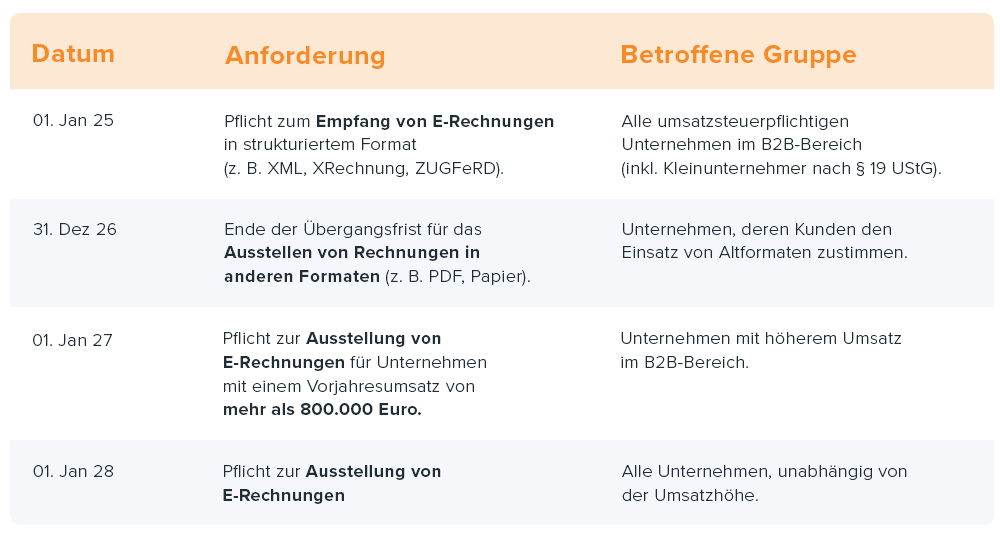

E-invoicing is being introduced gradually. From January 1, 2025, all companies subject to VAT must be able to receive e-invoices. The previous priority of paper invoices will no longer apply.

Transition periods for e-invoicing

There are transitional periods for issuing e-invoices. Companies may continue to use paper invoices or PDFs until the end of 2026, provided the recipient agrees. From 2027, companies with an annual turnover of more than 800,000 euros will be obliged to only issue e-invoices. Smaller companies have until the end of 2027 to convert their processes accordingly. From 2028, the e-invoicing obligation will finally apply to all B2B companies.

This staggered introduction is intended to ensure that smaller companies in particular have enough time to adapt to the new requirements. However, both from a regulatory perspective and for the efficiency of your accounting processes, it is worth integrating e-invoicing into your workflows as early as possible. This is because you save a lot of time and effort when invoices are automatically validated, archived and processed. At the same time, you meet all legal requirements – without stress or last-minute adjustments. Start the changeover now and take the opportunity to optimize your processes.

All posts in the blog series on the e-invoicing obligation at a glance:

Part 2: E-invoicing in just a few steps

Part 3: Expert tips: The e-invoice with JERA and GREYHOUND