Studies put the average conversion rate of online stores (excluding Amazon) at two to three percent. This means that for every 100 visits generated, only a maximum of three transactions are achieved. Anyone pursuing a growth strategy now has a choice. Either measures are introduced to increase the average transaction volume / shopping baskets or the focus is also placed on reducing the purchase abandonment rate.

What are the reasons for the high purchase abandonment rates?

There are many reasons for this – but one reason is mentioned particularly frequently: Around 20 percent of online purchases are abandoned if the desired payment method is not offered in the online store. (Source: Internethandel from 06.02.2014)

Purchase on account remains the most popular payment method for consumers.

Especially when it comes to the conversion rate, the choice of preferred payment method is an important criterion for many consumers. Across all countries, pay by invoice is the payment method that consumers rate best. This is also confirmed by the study “Internet payment transactions from the perspective of consumers in D-A-CH – IZV 11” by ECC Cologne and Aschaffenburg University of Applied Sciences. Listing this payment option can therefore also increase the conversion rate. But at what cost and risk?

On the merchant side, the greatest risk with purchase on account is that customers do not pay for the ordered goods after receiving them. However, online retailers are not defenceless when it comes to delivering this payment default. If you want to introduce purchase on account in your online store, you basically have two options to minimize the risks by outsourcing to a payment provider or through professional risk management in an in-house solution.

The decision to realize purchase on account with or without an external service provider

Outsourcing usually costs between two and five percent of the value of goods, whereas the process of an in-house solution costs up to three percent of the value of goods, according to a recent study by the EHI Retail Institute. Margins are very low in online business anyway, but the direct costs and the risk to be borne are not the only decisive factors to be considered.

Risk management for purchase on account

Digitalization is changing people’s behaviour, and the growth in online business is placing ever higher demands on risk management and fraud prevention.

The aim is to enable the customer to make a purchase without prepayment wherever possible. For purchase on account, for example, the credit rating is a basic instrument. As this is a risky payment method for the merchant, the credit check is justifiable under data protection law, provided the customer has been informed of this in advance.

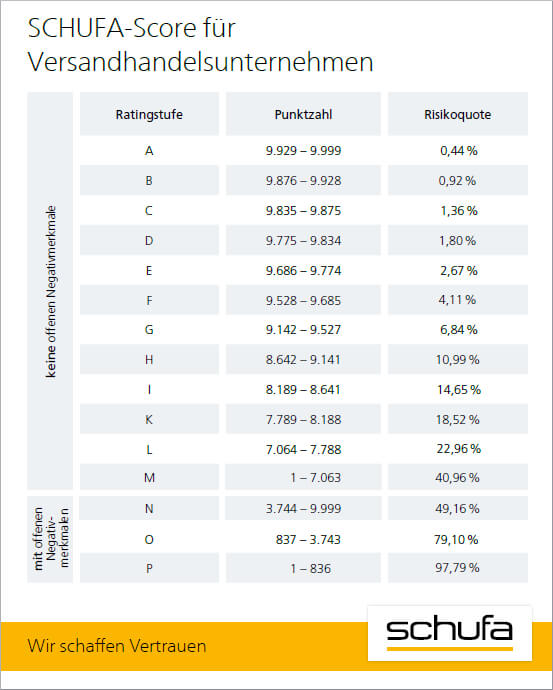

Credit rating – on the basis of valid and unique data

With 797 million individual pieces of data on 66.4 million natural persons and 5.2 million companies, SCHUFA offers a unique data basis and is therefore a reliable partner for assessing creditworthiness. The SCHUFA mail order score helps to minimize the risk of non-payment and to tap unused sales and earnings potential. A separate contract with SCHUFA Holding AG is required to obtain the SCHUFA products.

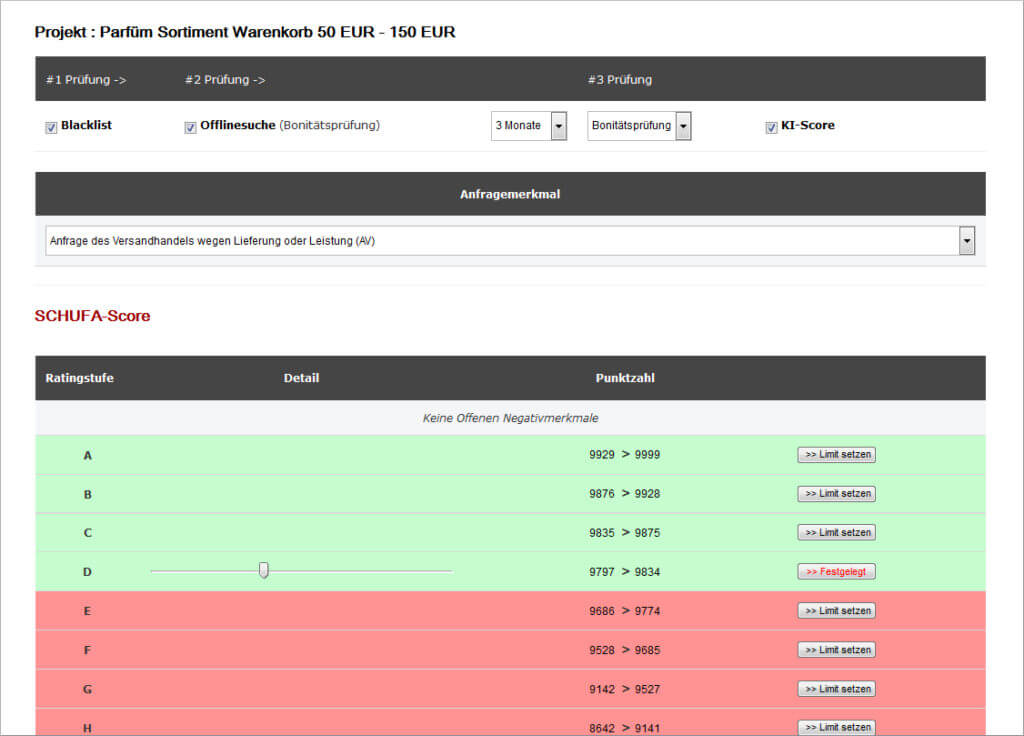

Individual risk management in your JTL-Shop with EAP-BoniGateway

Product range, target group and individual wishes of the shop manager require an individual risk configuration per shop.

The possibility of regular evaluations of sales, defaults and customer feedback for subsequent fine-tuning of the risk configuration are prerequisites for professional risk management.

All requirements were developed together with JTL-Shop operators and mapped in the EAP-BoniGateway for SCHUFA integration.

The core functions here include the shopping cart-dependent credit check based on the SCHUFA mail order score and the option of using other individual criteria such as customer groups or your own blacklists.

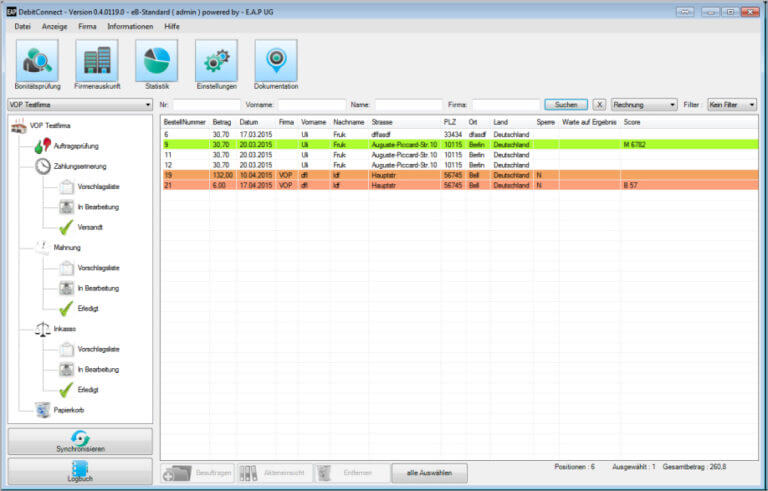

The opportunity with EAP-DebitConnect for your JTL-Wawi

The natural progression is the expansion and integration of risk management with the CRM strategy and holistic receivables management.

“Many years of practice show that nothing is more effective than avoiding a payment default before it even arises.”

If a payment default occurs, EAP-DebitConnect is an effective tool and offers reminders and debt collection in real time. This add-on for JTL-Wawi was also developed in close cooperation with JTL-Shop operators and offers maximum work simplification and cost savings. It is possible to map the complete dunning process from the payment reminder or to work only in addition to JTL-Wawi.

Many other functions, as well as the seamless integration of the information into the customer’s individual score, enable holistic receivables management with EAP-DebitConnect.

Outlook – new version for JTL-Connect on 26.08.2016

After our two-year development and testing phase, we would like to take this opportunity to thank our beta testers and look forward to presenting various enhancements in our release 1.0 for this year’s JTL-Connect.

The new functions are interlinked at all levels and enable optimal utilization of the given resources.

JTL software – a strong partner

The first contact between V.O.P and JTL came about rather by chance, when a customer asked “if we could help him develop a plugin”. Equipped with a SCHUFA interface at the time, initial discussions with Thomas Lisson, founder of JTL-Software GmbH, revealed not only the potential for us, but also how helpful our solutions would be for JTL-Shop operators. V.O.P has been an official JTL technology partner since 2014 and was able to realize all the sketches and ideas from the initial brainstorming sessions.

One point was clear to Thomas Lisson from the outset – our product and our services had to be a 100 percent fit for JTL’s customer base and under no circumstances, not even in terms of receivables management, should they represent a cost risk for a JTL-Shop operator.

The result is the JTL framework agreement which contains a cost assumption agreement in addition to 100 percent payment of the realized claims. This means no cost risk for you.

Your path to your own risk/receivables management

Are you interested in our products? We would be happy to advise you on the integration of individual or all modules into your company processes. A free version, which already contains a large number of functions, is available for download from our product page www.eaponline.de.

If you would like to use the complete package including EAP-BoniGateway, the EAP-DebitConnect Premium license is the cheapest option.

Tip: The EAP-DebitConnect Premium license is also available from selected JTL service partners who offer interesting software bundles.