E-invoicing has been mandatory in the B2B sector since January 1, 2025 – a topic that most of you had to get to grips with first. While numerous providers advertised their solution in the beginning, communication has since become much quieter. However, the requirements remain high and implementation in everyday life poses challenges for many retailers. In this article, you will get an overview of typical stumbling blocks – and what you should pay attention to now when creating and processing e-invoices.

What does the law say?

Although the topic of e-billing seems to have fallen somewhat out of the public spotlight at the moment, the legal requirements still apply without restriction.

- For business transactions between companies (B2B) within Germany, both the invoice issuer and the invoice recipient must be able to receive e-invoices. This obligation applies to all companies with a registered office in Germany – or, if there is no registered office, with a domicile or habitual residence in Germany. The same applies to the areas specified in Section 1 (3) UStG.

- Only an invoice created in XML format is accepted as an e-invoice. The structure for this is specified in EU-DIN 16931. All other formats, e.g. in paper form or as a PDF, are regarded as “other invoices” and do not entitle to input tax deduction.

- The invoice in XML format may not be changed and must be archived in the format in which it was received. In the event of a tax audit, the invoice must be made available in XML format. To ensure this, the invoice data records must be checked electronically. After a technical and factual check, they receive an electronic identifier that identifies the data record as formally and factually correct, the so-called validation.

IMPORTANT: Only a validated and archived e-invoice entitles you to deduct input tax!

Exceptions to this obligation only apply in a few cases, namely:

- for tax-free transactions according to §4 number 8 to 29 UstG

- for invoice amounts up to 250 euros

- and for tickets (e.g. for local public transport).

The expert talk on the subject of e-invoices: Ulrich Pöhner, Sascha Lammers from GREYHOUND and Johannes Seidel from JERA talk about everything retailers need to know.

Typical stumbling blocks from practice

In the first few months of this year, we were able to gain a lot of experience in the area of e-invoicing and have summarized a few frequently asked questions:

Outgoing invoices

The creation of outgoing invoices seems simple at first glance. However, some questions arise in detail.

Incoming invoices

Difficulties also occur time and again with incoming invoices – often only at second glance. We have summarized the most common challenges for you here.

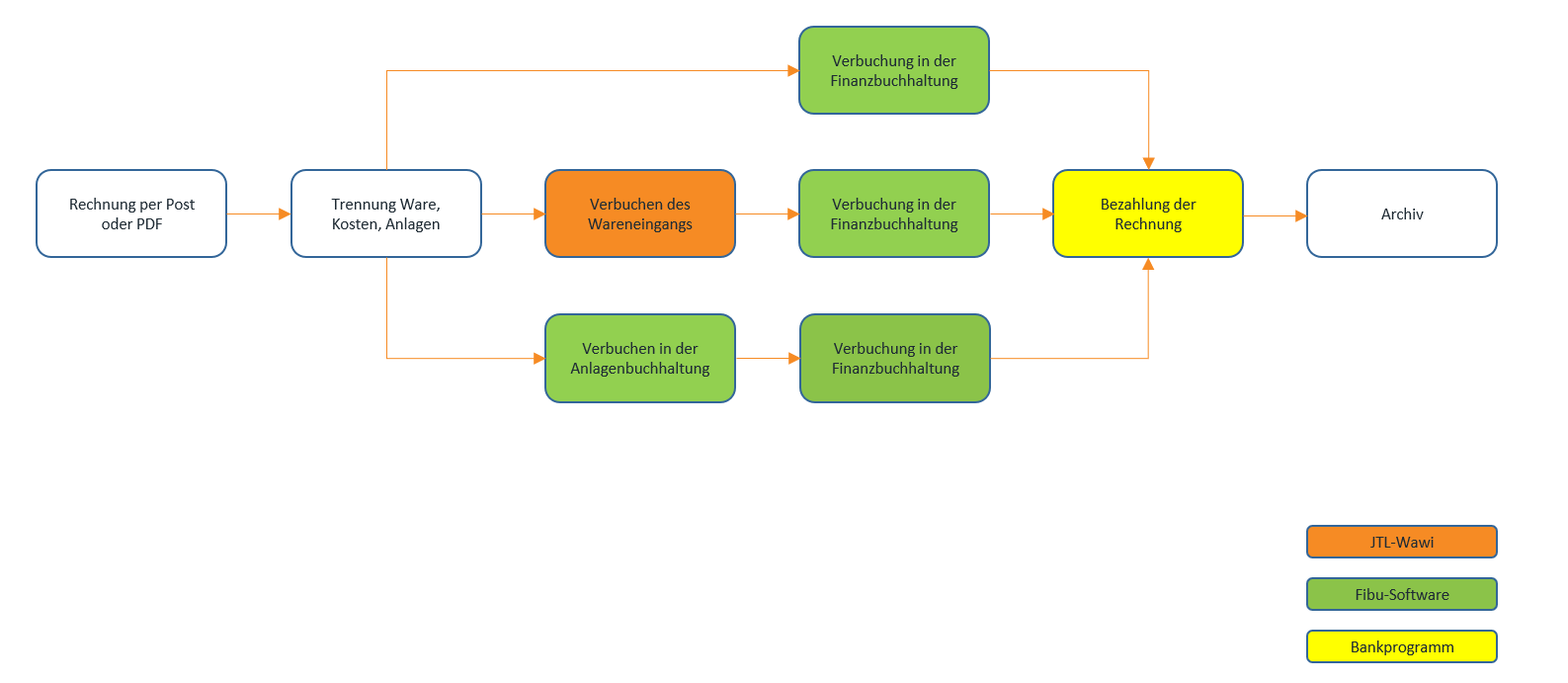

Above you can see the classic invoice receipt posting process: receipt of the invoice, payment and posting in financial accounting.

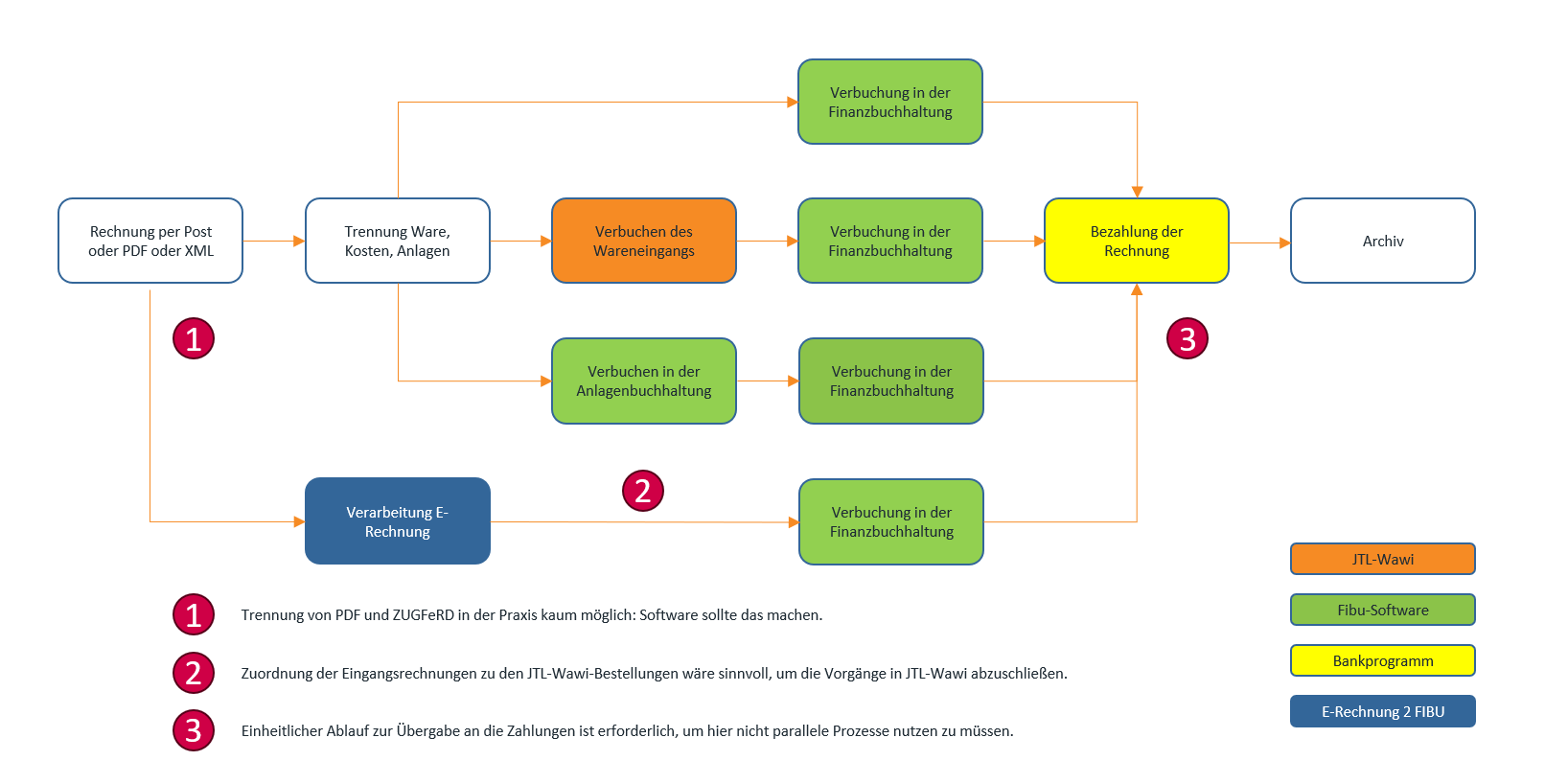

Below is an illustration of how the e-invoice creates a second process strand that drives digital processing but still has to be merged with the conventional invoice receipt process in the final stage.

Successful implementation with the right preparation

E-billing is here to stay – and presents many retailers with new challenges. Our experience to date shows that Those who know the technical and content requirements and adapt their processes accordingly can master the changeover well. Above all, it is important that the ERP system used supports both XML and ZUGFeRD, that content is filled correctly and that the internal processes for incoming invoices are clearly regulated.

Even if getting started can involve additional effort, investing in well thought-out e-invoice processes pays off in the long term – especially in terms of efficiency, transparency and legal security.

With the JERA E-Invoice 2 FIBU add-on, you can create and process e-invoices in a legally compliant manner – including validation, archiving and transfer to the accounting department.

We have already created an extensive blog series on the topic of mandatory e-invoicing. You can find all the articles here:

Part 1: E-invoicing obligation 2025: everything online retailers need to know

Part 2: E-billing in just a few steps

Part 3: Expert tips: The e-bill with JERA and GREYHOUND